We believe everything you do as you venture into retirement should focus on risk management . Familiarize yourself with what risks pose the biggest threat. For example, do you know what sequence of return risk means? Failure to put a plan in place to account for sequence of return risk can mean a significant reduction in your retirement funds later down the road.

Sequence of return risk arises from those cycles of good years and bad ones. You cannot ignore it, particularly if you plan to retire now and will begin withdrawing money from your investments. You need to understand its potential to wreck your retirement plans. “Don’t worry, you’re fine,” a misguided advisor may tell you. “Look here, your investment averaged 8 percent over the last three decades, so you can take out 5 percent and even increase it for inflation at 3 percent, no problem.” But it’s a big problem if you encounter some bad years early on.

A bad year or two may not have hurt you during the years when you made no withdrawals or were contributing to the account, because a good year or two could turn that around. Now, if those bad years come at the same time that you are siphoning money away for your income needs, the good years later on may not be able to overcome the hit. When choosing an investment for your portfolio, a high historical average should no longer be a key factor. That average rate of return is measured simply as an average over the years. Some are good years, some less so. In Distribution Land, you won’t have the investment long enough to care about the average return. Your advisor should be accounting for sequence of return risk by implementing different money management strategies.

Do you know how your current advisor is paid? What should you ask about fees and commissions when you are searching for an advisor? These are crucial questions. You need to understand how advisors make money so that you can weigh the advice that you receive. Overall, some are paid commissions on products they sell. Some charge a fee for impartial service. Others make their money with a combination of commissions and fees.

Many advisors today are commission-based, a model that has long existed. If you buy something from them, they receive a fee for services based on a percentage of the dollar amount of the sale. That’s how the majority of insurance products and investments such as mutual funds still are handled.

As for those advisors who tell you that they work for you at no charge because their company pays the commission, ask yourself this: If they do all that work for you for nothing, how do they feed their kids and pay the mortgage? You have to buy something for the commissions to flow, and you may hear recommendations that will compensate them.

Fee-based planners make their money by creating a financial strategy for you. Those who also sell products or manage assets would like you to implement that plan with them, but you are free to take the plan elsewhere to put it into action. The licensing of fee advisors requires that they act in a fiduciary capacity—that is, in your best interest as would be considered prudent according to a court of law.

That’s why you may want to pay separately for planning services. The advisor has no vested interest or bias. He or she gets paid for the work, and you can implement the strategies as you please, if at all. Thinking it might be time for a second opinion on your financial plan? Go to www.mysecondopiniontoday.com for a free consultation and portfolio review to see if you are headed in the right direction.

The costs of medical and long-term care are often underestimated, and some retirees do not even consider them—and yet they are one of the primary reasons that people run short of money in retirement.

According to a May 7, 2012 survey, conducted by Harris Interactive for Nationwide Financial, nearly half of high-net-worth Americans who are close to retirement are “terrified” of what health care costs could do to their retirement plans. But 38 percent of those surveyed said that they haven’t discussed retirement health-care costs with a financial advisor, in part because they are unsure as to whether their advisor is knowledgeable about the issue. This is not a good sign.

To put it in perspective, several years of care can wipe out half a million dollars of life savings. “Well, it’s not going to happen to me,” you may think, but statistically, it could. The lifetime chance that someone who buys a policy at age 60 will use their policy before they die is 50 percent. A more responsible approach is to analyze the cost and look for ways to fund it*.

People may think they will need to pay for the cost of insurance out of their cash flow—and as a result, they worry that they won’t be able to go out to dinner or visit the grandkids or play a round of golf. But often they do have money, perhaps half a million or so, so the fact that they have assets is what raises the issue. If they had no money, then Medicaid could be their plan.

Ultimately, medical and long-term care should be considered and planned for.

A good advisor will talk about the meaning of money in relation to your goals and dreams. You need to share such things before the talk turns to finances, or an advisor can’t truly know how to help. If the first thing an advisor does is ask to look at your statements, says Mitch Anthony, author of The New Retirementality, you should head for the door.

Everything that happens in people’s lives affects their finances. At Family Wealth Management, we use a program called Money Quotient that helps us get to people’s core values and beliefs and hopes for accomplishment. “Putting money in the context of life™” is Money Quotient’s motto.

The Money Quotient tolls can help with planning your immediate, short range, and long-term goals. We calculate how much those goals would cost, and we try to build an income plan that is designed to accommodate them. If you’re out to top the S&P 500, that’s not what a goal is.

As part of the process, we ask what you want in life. What’s important to you? If it’s a vacation each year with the kids and grandkids, we build that into your plan. If it’s an education scholarship to your alma mater, we set that aside. Whatever you wish to achieve, we calculate it into the target rate of return that would be needed to fulfill it. We won’t go after a 40 percent return just to beat some benchmark. Why would it matter?

When people don’t have a focus, they can wind up competing against financial benchmarks. But when they have a clear vision of their retirement goals, they can start planning to reach those goals instead. That’s why it’s important to start the planning at least five years before retirement, so you can lay the groundwork and begin building.

With an IRA, required distributions are designed so that theoretically, your distribution period is always greater than your age*, presuming a normal growth rate. So for many retirees, the money doesn’t run out. There is money left for heirs. It’s important to consider how that money is passed on.

The beneficiary of what is called “an inherited IRA” can opt to continue the tax-deferred growth; the rules for required distributions allow for such a “stretch” provision**. He or she can take distributions over a fixed period of time, based on life expectancy. For example, a 20-year-old beneficiary can take payments over 63 additional years. Special rules apply to spousal beneficiaries after that.

A word of caution, though: Given the choice of a lump sum or tax-deferred distribution (and I have seen this happen many times), most heirs seem to know only four words: “Show me the money.” If you suspect that will be the case, it’s possible, to name a trust as the beneficiary of your IRA to establish some control over how distributions will be taken after your death. You should consider whether family situations call for such action.

Most heirs will not know that a stretch is available to them—and if they do, they could fail to get the full benefit from it. IRA owners can do themselves and their heirs a big favor by setting this up in advance, in some way, shape, or fashion. They could reach out to the heirs, while the account owner is still alive, and explain the distributions available to them and to whom they can go to for guidance when the time comes for distribution.

Mutual of Omaha Investor Services, Inc. and its representatives do not provide tax or legal advice; therefore it is important to coordinate with your tax or legal advisor regarding your specific situation.

In my opinion, the financial planning industry in general tends to be good at dating, but less successful in marriage. You will find “advisors” who tell you what you want to hear just to get you as a client. Then they’re in pursuit of someone else. At Family Wealth Management (www.familywealthadvisory.com), we strive to provide diligent follow-up care—four quarterly meetings each year, preferably. The objective for each meeting is to reduce risks, focus on opportunities, and continue working so that we continue to tap into the client’s strengths and stay true to his or her values.

A lot of people in our industry sell stuff, but they may not do financial planning. Retirement planning may be more complicated than investing to accumulate assets. A good planner needs to analyze the client’s expectations and finances and understand all the major risks that retirees face. As you head into retirement, you should search for somebody who cares about your unique situation. See our previous blog post about this.

And that somebody isn’t likely to be the stockbroker who wants to direct you to all those hot mutual funds. The United States has about 1.3 million licensed stockbrokers and insurance agents, and they may call themselves financial planners, but there are only about 25,000 Certified Financial Planners™, or CFPs, who have completed the CFP certification process.

In your accumulation years, when you were adding dollars and buying equities at a bargain, you benefited from what is known as dollar-cost averaging: the technique of buying a fixed dollar amount of a particular investment on a regular schedule, regardless of the share price. More shares are purchased when prices are low, and fewer shares are bought when prices are high. Eventually, the average cost per share of the security will become smaller and smaller. Dollar cost averaging lessens the risk of investing a large amount in a single investment at the wrong time.

For example, you decide to purchase $100 worth of XYZ each month for three months. In January, XYZ is worth $33, so you buy three shares. In February, XYZ is worth $25, so you buy four additional shares. Finally, in March, XYZ is worth $20, so you buy five shares. In total, you purchased 12 shares for an average price of approximately $25 each.

Now, in retirement,as shares go down in value, you have to sell more of them from your account to obtain the same income. It’s dollar-cost averaging in reverse. Think of it as dollar-cost ravaging. See our previous post concerning this.

For the most part, 401(k) plans have replaced pensions as the prevailing vehicle for people’s retirement. But surveys and studies show some very bleak numbers. The balances in 401(k)s and IRAs may not be nearly enough to pay for comfortable retirements, as the previous generation’s pensions once did. And today, few companies offer pensions.

Why is it possible that 401(k)s and IRAs may not provide as much retirement income as a pension? There are several reasons. First, not all companies offer 401(k) plans, just as some companies did not offer pensions. However, investors who do contribute to 401(k) plans often are unaware of the array of annual charges, such as administration fees, sales charges, management fees, and individual services that they are paying and that are siphoning away their earnings. Fees aren’t “hidden” so much as they’re judiciously disclosed. Many people simply don’t know how or where to look for those fees.

Fees, regardless of how conspicuously they’re disclosed, should be but one criterion you pick for your 401(k) investments. Look at asset class, management’s relative competence, and track record first. Each of them will have a far greater impact on your long-term returns than fees. If you aren’t sure what fees you are paying or how your 401(k) stacks up, seek out the advice of a professional. See how Family Wealth Management can help at www.familywealthadvisory.com.

According to an AARP study*, more retirees fear running out of money than they fear death. You deserve to have power over your finances and the opportunity to live a life unencumbered by financial worry.

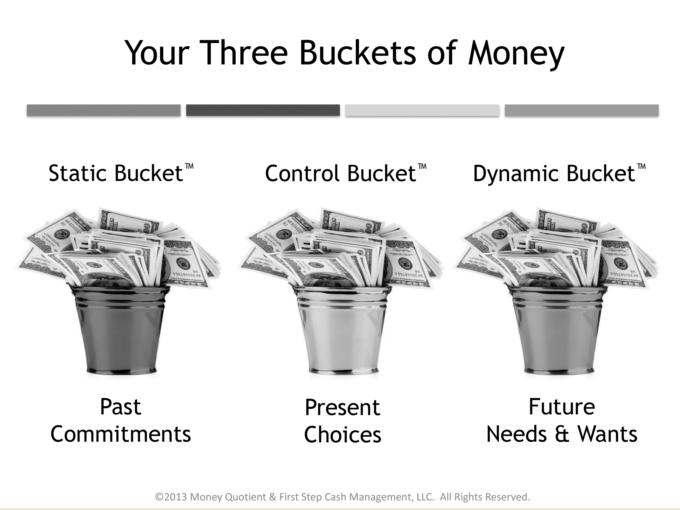

The First Step Cash Management system** can help ease some financial worries as it allows cash to flow into three accounts or “buckets.” Each of the three buckets holds a specific type of money, and each type of money has a specific use or purpose. This system aids in tracking your spending and knowing where your money is going.

1. The Static Account™ bucket holds money that has been spent or has agreed to be spent at some point in the past, such as mortgage, auto loans, credit card debt, insurance, and utilities.

2. The Control Account™ bucket contains money that will be spent within the next seven days. This account includes daily needs like groceries, pet care, clothing, etc.

3. The Dynamic Account™ bucket stores money that will be spent in the future on things such as charitable giving, debt reduction, vacation, and gifts.

For retirees who feel overwhelmed by the many decisions they face as they enter retirement, a bucket strategy similar to the envelope system that their parents may have used back in the day, may help them divide what they see as one large stress-inducing problem into smaller, more manageable pieces.

*Running Out of Money Worse Th an Death – by: Carole Fleck: AARP Bulletin, July 1, 2010 **First Step Cash Management is owned by Th e Planning Center Inc. and Distributed by Money Quotient, NP

There are two main types of guaranteed income products, a guaranteed income annuity and a reverse mortgage. A guaranteed income annuity is essentially a product where, for an initial investment, an individual receives a guaranteed income stream for the remainder of his or her life. With a reverse mortgage, homeowners can receive monthly payments from the reverse-mortgage lender for the remainder of their lives. At the time of their death, the money they have received must be repaid to the lender by the estate, or possession of the house is granted to the lender. Is a guaranteed income product right for you?

PROS Can essentially function like a personal pension plan by providing consistent monthly income payments to retirees in order to help individuals plan their cash flow needs. May also make budgeting simpler because monthly cash flow is known in advance and is not dependent on financial market conditions.

CONS Individuals are generally locked into a relatively low rate of return. This means that in exchange for a guarantee of safety and lifetime income an individual sacrifices the possibility of higher returns.

Guaranteed-income products often suffer from a lack of liquidity and may not keep pace with the rate of inflation.

If you are considering guaranteed income products, comparison-shopping is absolutely vital. Also, consider general health and life expectancy, if a spouse will be included in the contract, and if you want to leave an inheritance, as all of these factors can impact whether or not guaranteed income products are a good choice for your financial future.

Annuities are long-term investments designed for retirement purposes. Distributions are subject to income tax and, if taken prior to age 59½, a 10% federal tax penalty may apply. The annuity may be subject to lengthy surrender periods and early withdrawals subject to surrender charges. Guarantees are backed by the claims-paying ability of the issuer.

The decision to take out a reverse mortgage can be a difficult one to make. The AARP, an American organization dedicated to protecting the elderly and retired, has extensive free resources designed to educate senior citizens about potentially unjust lending practices. Anyone considering a reverse mortgage should gather as much information as possible before carefully deciding whether a reverse mortgage is appropriate.

We believe everything you do as you venture into retirement should focus on risk management . Familiarize yourself with what risks pose the biggest threat. For example, do you know what sequence of return risk means? Failure to put a plan in place to account for sequence of return risk can mean a significant reduction in your retirement funds later down the road.

We believe everything you do as you venture into retirement should focus on risk management . Familiarize yourself with what risks pose the biggest threat. For example, do you know what sequence of return risk means? Failure to put a plan in place to account for sequence of return risk can mean a significant reduction in your retirement funds later down the road.