In retirement ROI stands for reliability of income*, a far greater concern in these years than return on investments. You can’t effectively chase both at the same time. But you can pursue both goals if you compartmentalize your money based on short-term, medium-term, and long-term goals.

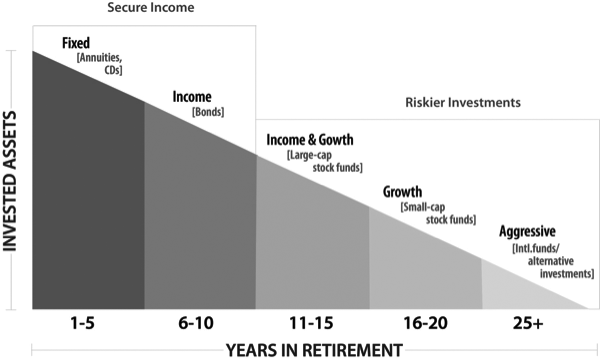

You may have seen what is called the “risk pyramid,” rising from conservative fixed investments at the bottom to more aggressive growth vehicles at the top. Imagine that pyramid toppled on its side. You would have, at the left, the widest part—the fixed investments. At the right you would have the growth investments. This pyramid on its side is another way to visualize the time sequences in certain types of income planning.

How does it work? Reliable sources of income such as Social Security, perhaps a pension, and income from a job are calculated first. Then we put in the targeted growth rate, and we use conservative figures. Then we set up four to six segments, usually in five-year payout periods. The first bucket takes you to five years into retirement; the second takes you to ten years; and so on. This process supports the use of the Time Segment Model.

If this sounds like a good plan for your retirement needs, get in touch at www.familywealthadvisory.com for more information.

*ROI Reliability of Income is a registered trademark of Wealth2k, Inc. Used with permission.

The tactic of withdrawing from an account that rises or falls with the market can be debilitating to your wealth. You are at the mercy of sequence of return risk (the potential consequences of a bad sequence of returns) at the time you begin withdrawing money from your investments (reverse dollar cost averaging).

If those don’t drain your account, you will most likely deplete it entirely just by living too long.

Adding guaranteed income products to a traditionally diversified portfolio may provide the potential to capture a portion of market gains, while potentially limiting losses when the market experiences a downturn. Using this model, explained below, can also help.

Time Segment Model

A more disciplined structure for creating retirement income. This approach is designed to spread your portfolio across multiple accounts, each designed to produce income over a certain period of time. How each account is invested depends on how soon the money is to be used. Typically, the initial segments are for immediate needs and may therefore be allocated conservatively in fixed rate or even guaranteed investment products such as certificates of deposit or immediate annuities that may not be subject to a fluctuation in principal. Segments designated for later use can be invested more aggressively. Since they won’t be touched for a while, they have time to overcome market corrections. Over time the aggressive segments will be shifted to more conservative products as retirement savings are used.

Using this model to build your investment portfolio may allow for continued steady income instead of just playing the stock market game of chance. If you aren’t sure that your current plan uses this model, maybe it’s time for a second opinion. Schedule yours at www.mysecondopiniontoday.com for a no obligation assessment of your current portfolio.

All investing involves risk, including possible loss of principal.

Despite the risks you might now know of like, dollar cost ravaging and inflation, some advisors still put everything in a lump sum for systematic withdrawals. They will craft a portfolio that seems beautiful in its asset allocation, but really the income derives from withdrawing a percentage of the portfolio. And that puts the entire portfolio at risk.

Let’s say it’s in a 60-40 mix of stocks and bonds, and the market tumbles. “You don’t have all your eggs in one basket,” you will hear, and that’s the line of “modern portfolio theory,” which isn’t so modern anymore, having been around for 60 years or so. It came from a time when the United States was the dominant investment player in the world. Today’s global economy behaves differently. Simply put, Modern Portfolio Theory tells you that diversification leads to retirement success. But don’t feel too reassured. Diversification is too often defined as stocks, bonds and cash. In times of extreme volatility, investments get more closely correlated to one another. Often portfolios don’t include other types of investments or downside protection strategies that truly help to build a diversified portfolio. Guaranteed income products may be an effective alternative investment.

An investment strategy that requires luck—luck that you will retire into a bull market and not a bear—isn’t much better than a strategy that requires flipping a coin. An appropriate strategy for you depends on your investment objectives, risk tolerance and time horizon.

Imagine that you have a 200-piece jigsaw puzzle scattered in front of you. Where would you start? When I ask people that, most say they would start at the corners where they figure it’s easier to piece together all those interlocking shapes. Likewise, many people just dump their box of investments on an advisor’s table and shift them around, trying this investment here, and that one there, and hoping that eventually things might fall into place.

But how about first taking a good look at the picture on the cover of the box? Before you start working on the pieces, you need to have the big view. You should work with an advisor who will make sure you get the perspective you need so that your investment strategy makes sense for you and is designed to advance your goals.

Finding an advisor you can trust to give you direction, not just do what you ask, may result in a much more secure retirement future. Is your puzzle pieced together with the big picture in mind? Consider getting a second opinion on your current investment portfolio and schedule a free consultation at www.mysecondopiniontoday.com.

“Many people are so occupied with getting out of a career trap that they seem to care little about what happens after they leave their jobs. Too many people retire to nothing and then wonder why they feel empty and disenchanted.” From “Comfort Zones”, by Elwood Chapman and Marion Haynes

The point being, if you would like to avoid feeling empty and disenchanted, you shouldn’t just wing it. Yet it seems that is how a lot of people approach retirement. They wait until they’re into it before they start planning. As a result, things may not work out as well as they would if they had addressed them earlier, and they can end up unhappy and disillusioned. They had grown weary of the daily race of their workaday life, but they may find retirement filled with new anxieties. They can’t seem to slow down.

By deciding your destination up front, you can set your own pace. You will know how much income you need to accomplish your goals and still live comfortably the rest of your days. The “Retirement Red Zone,” as Prudential calls it, should begin five years prior, and probably ten years if you are a business owner. Many people have an investment plan but no overall financial plan.

Visualize the lifestyle that you will find most satisfying and fulfilling. Give your life direction by setting goals so you can anticipate, plan and prepare. Focus on expectations. Start now; download a free chapter of my book DistributionLand (www.distributionland.com) for the strategies and risks to consider as you begin the journey.

I once asked an estate-planning attorney how he got his best clients. “It’s the people who try doing it themselves first,” he answered. “They try to do their own planning, and I get more business by fixing things for people than I do from doing it right for them to begin with.”

There can be a disconnect between having information and knowing what to do with it. When it comes to investing, however, some people think that if they have obtained information, gleaned perhaps from the Internet, then they also have knowledge and wisdom. In my opinion, they generally do not. Investing wisely requires expertise and experience.

In Accumulation Land do-it-yourself investing might be considered a fun hobby, something to dabble in occasionally. And that’s okay because remember, you have time on your side then. But as you approach retirement, the stakes are higher and the game changes. What was once a hobby may need more insight and true knowledge. Without time to recover from your mistakes is it worth it to dabble away your hard earned money?

Do it right from the start. Visit www.mysecondopiniontoday.com to schedule a free consultation. Make sure your current financial plan is ready for retirement.

When it comes to long-term care, some people still are thinking, “Well, I’ll just depend on Medicare and maybe Medicaid.” They don’t realize how limited Medicare is in covering certain types of benefits. For example, to get any coverage for a nursing facility, you have to be in the hospital for at least three days, then be discharged and admitted to the facility within 30 days for the same condition. If you can jump through those hoops of fire, then you can get 100 days of coverage, for which you will still pay 20 percent. And after that, it’s done.

The government has made it explicitly clear that it doesn’t pay for long-term care—it’s clear in brochures and other publications. Medicare is not a solution for long-term care. Medicare should be viewed like health insurance.

The use of Medicaid to provide care has also been greatly restricted. The policies are clear: Medicaid is not to be used as a solution for wealthy people to transfer their money and save it. Medicaid was created for the purpose of providing medical assistance to low-income Americans. Some people feel too proud to go on Medicaid, even though they lack assets and can’t afford long-term care insurance. Meanwhile, some wealthy people are trying to get on those rolls. They try to reposition their assets to make themselves indigent on paper—but it’s much harder to accomplish that than it was 10 or 15 years ago.

These are complex programs for care that require expert knowledge in understanding terms, applications, eligibility, and even strategies for maximizing use. Talk to your financial advisor about long-term care and insurance and what might work best for your needs.

At some point during your retirement years, you may find it advantageous to convert your traditional IRA to a Roth IRA, in which the taxes are paid up front and the eventual distribution comes to you tax-free.

Converting is not that big of an issue, technically. It can be a big issue financially, however, because you face the prospect of paying those taxes in the year of conversion. Above all, however, the conversion has to make sense.

Consider this scenario: For a married couple who want to convert to a Roth but who do not have the money to pay the taxes, one strategy may be to purchase a life insurance policy that we can use is a spousal Roth conversion.

Let’s say the husband and wife are both living, it’s the husband’s IRA account, and the couple does not need the money in the account. When it comes time to take the required minimum distributions, one option may be to purchase a life insurance policy on the husband in the amount projected to be necessary to pay the taxes upon his death so that his wife can convert the account to a tax-free Roth.

Let’s say that it would require $100,000 in taxes to convert a $400,000 account. When the husband dies, the wife inherits the $400,000, and she also receives a $100,000 death benefit. She could use the life insurance money to pay the taxes, and now she has a $400,000 Roth. That’s a way to accomplish a conversion without having to come up with the money right away.

Make sure you discuss with your financial advisor if converting to a Roth IRA makes sense for you and your family. This approach may not be right for everyone. Visit www.familywealthadvisory.com for more resources and advice on financial planning.

Years ago, a farmer and I were discussing long-term care insurance. He was having trouble grasping why he needed it and how he could pay for it.

“Let me ask you something,” I said. “I’m looking out at your fields. I see all your cows…”

“Yes, that’s everything I own,” he said.

“And out in that field is a rat hole somewhere, I’d assume; would that be correct?”

“Yep, that’d be correct,” he said.

“Then let’s consider the nursing home, a rat hole. Is that ok with you?”

“Yep, that sounds about right,” he laughed.

“Well, if you get sick and need to go into a nursing home,” I said, “you might have to sell off a fifth of your herd every year for five years until they’re all gone—or else you can set aside some of the milk now from some of the cows so that you can protect the whole herd.”

“OK,” he said. “I get it. You just want me to take a little bit of interest off some of my CDs and buy long-term care insurance so I don’t lose it all.”

He finally understood what I had been trying to tell him. He would be better off giving up some of the milk, or else he’d be risking the whole herd. Do you have a plan for long-term care insurance? If not, it might be time to seek out some advice on where to start, visit www.familywealthadvisory.com for information and resources.

As you near retirement, it can feel as if you are climbing Mount Everest and just need to hold on long enough to reach the summit. Once there, you hope to behold that glorious view of Distribution Land shimmering below you, stretching out to the horizon.

But consider this: A great many of those who have perished on Mount Everest met their fate on the descent, not the ascent. A mountain climber needs an entirely different set of skills on the way down. Some people need a competent guide on both sides of the mountain—someone who has been there many times before and knows the terrain and conditions. Otherwise, a sudden change in the weather or the wind could do you in.

Here are the potential enemies you could face in Distribution Land. Don’t let them surprise you on your retirement journey:

A financial advisor can create a strategy designed to help you come down the slope safely and inspire a sense of accomplishment. Learn more about these risks and the strategies for overcoming them in my book, DistributionLand .

In retirement ROI stands for reliability of income*, a far greater concern in these years than return on investments. You can’t effectively chase both at the same time. But you can pursue both goals if you compartmentalize your money based on short-term, medium-term, and long-term goals.

In retirement ROI stands for reliability of income*, a far greater concern in these years than return on investments. You can’t effectively chase both at the same time. But you can pursue both goals if you compartmentalize your money based on short-term, medium-term, and long-term goals.