We believe everything you do as you venture into retirement should focus on risk management . Familiarize yourself with what risks pose the biggest threat. For example, do you know what sequence of return risk means? Failure to put a plan in place to account for sequence of return risk can mean a significant reduction in your retirement funds later down the road.

We believe everything you do as you venture into retirement should focus on risk management . Familiarize yourself with what risks pose the biggest threat. For example, do you know what sequence of return risk means? Failure to put a plan in place to account for sequence of return risk can mean a significant reduction in your retirement funds later down the road.

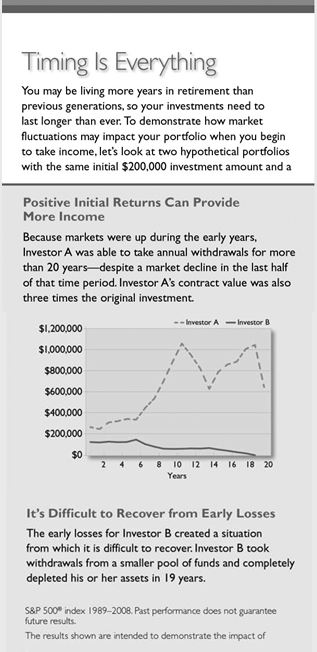

Sequence of return risk arises from those cycles of good years and bad ones. You cannot ignore it, particularly if you plan to retire now and will begin withdrawing money from your investments. You need to understand its potential to wreck your retirement plans. “Don’t worry, you’re fine,” a misguided advisor may tell you. “Look here, your investment averaged 8 percent over the last three decades, so you can take out 5 percent and even increase it for inflation at 3 percent, no problem.” But it’s a big problem if you encounter some bad years early on.

A bad year or two may not have hurt you during the years when you made no withdrawals or were contributing to the account, because a good year or two could turn that around. Now, if those bad years come at the same time that you are siphoning money away for your income needs, the good years later on may not be able to overcome the hit. When choosing an investment for your portfolio, a high historical average should no longer be a key factor. That average rate of return is measured simply as an average over the years. Some are good years, some less so. In Distribution Land, you won’t have the investment long enough to care about the average return. Your advisor should be accounting for sequence of return risk by implementing different money management strategies.