A woman once came to my office and opened her checkbook, telling me she had about $300,000 in her account. I asked why she felt she needed that much in a checking account.

“I have it there for emergencies,” she explained.

Few of us need access to all of our money at one time. Holding on to $300,000, a large amount of liquid assets, is often squandering potential. The price of liquidity is a low rate of return, and low growth means that inflation may overtake you.

Keeping direct access to all of your cash is a depression mentality: Some of those who endured hard times held on so tightly to their money that they sacrificed growth and eventually succumbed to the ravages of inflation. Remember your Grandma saying, “A dollar doesn’t buy what it used to buy?”

Be wary of the depression mentality as you approach retirement. If you have a hard time letting go of your liquidity, a financial advisor (www.familywealthadvisory.com) can help by creating a written retirement income plan that spells out the details and strives to make you feel comfortable with your potential future income growth.

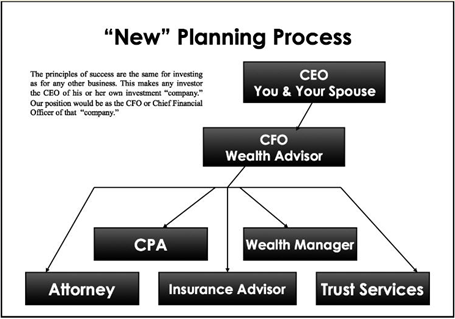

By hiring a good advisor, you could be gaining a world of expertise; however, you should still feel firmly in control of your destiny. You are the CEO or chief executive officer of your wealth. A good CEO hires a CFO or chief financial officer, who runs the daily affairs of the company. The CFO oversees and coordinates everything that requires planning and money with a written recommendation.

The goal is for you to feel free of financial worry so that you can spend your time focusing on what you enjoy. In my opinion, that’s so much better than the old planning model in which you are in the middle, and circling around you like the moons of Jupiter are all of your current advisors: your CPA, who calls you up every March to ask you where your receipts are; your lawyer, whom you haven’t seen in eight years since she handled your daughter’s auto accident; and your insurance agent, who calls too much, always at dinner time. Then don’t forget your investment advisor who hid under the desk in 2008 and wouldn’t answer the phone. If you have such a “team,” ask yourself when was the last time that they all got together and talked about your plan?

If you have a constellation of advisors, each will see just a piece of the jigsaw puzzle. None of them is likely to help you know how to fit those pieces together. That’s a job for a primary financial coordinator, your CFO, who will work to keep the big picture in mind. You should expect regular communication. Receive a free no obligation assessment of your retirement plan at www.mysecondopiniontoday.com. A good advisor will keep in touch so that you can make the adjustments to stay on course toward your goals. We can’t change the wind, but we certainly can trim the sails.

All of your career, you have been used to a paycheck coming in, and now in retirement that paycheck is gone. You have to create your own paycheck from your own resources, and that can feel quite unsettling. Social Security is uncertain and may be insufficient, and the days of private company pensions are nearly gone—replaced, for many people, by tax-deferred retirement plans, 401(k)s. Upon retirement, some fortunate people find themselves with a pile of money to manage somehow.

Imagine boarding a jet and heading to your seat, only to be told you are needed in the cockpit to fly the plane. That is what has happened in our workplace retirement system over the last 30 years. We have shifted from pension plans managed by professional financial pilots to 401(k) plans managed by passengers. You fuel the plane, you pilot the plane, and you land it. According to a 2014 research study conducted by the American College, 80% of respondents with nest eggs of at least $100,000 in assets, got an “F” on a test about managing retirement savings. It’s no surprise that many people are crashing.

In this post-pension era, you have to create your own cash flow. You have to take that pile and make it last for the rest of your life. Wondering how? Read up on retirement planning strategies. Start with a free chapter of Distribution Land (www.distributionland.com). You need to know some of the different ways to create an income stream so that you may feel more confident about your financial situation. And, you might consider adding the help of a professional co-pilot in a effort to land safely at your destination.

What You Don’t See: The Difference Between a Well-Laid Plan or Falling Short

I would like to share a story with you.

An accountant and his wife recently came to my office to prepare for their retirement in a few years. They had about $2.5 million in CDs and bonds, and they had figured out how much they wanted in retirement income. They presumed all was well. But my projection showed their portfolio in a death spiral by their early 80s.

“You know what that means, right?” I asked them. They risked running out of money.

“Yeah, it means I don’t believe it, how’s that?” the accountant said.

I showed him the numbers, and as a CPA he understood them, yet couldn’t quite grasp why this would be happening.

“Have you ever seen Jurassic Park?” I asked him.

“Sure. Dinosaurs gone bad.”

“Right. Remember the scene where the boy tells the archaeologist he wouldn’t be afraid of a raptor?” I asked. “The guy shows the kid a petrified claw and demonstrates how a raptor could shred him to pieces. But then he explains that the raptor that would be staring him down wouldn’t be the one he’d have to worry about. In fact, he wouldn’t have to worry about him at all. See, Velociraptors hunt in packs and it’s the ones to the sides that are going to kill you, and you’re never going to see them coming.”

The CPA furrowed his brow.

“You were scared,” I explained, “because you saw that market risk in front of you, staring you down. So you put all your money into CDs and bonds so you wouldn’t have to worry about market risk. But off to the side—and I don’t think you see it coming—are inflation and longevity as well as other risks that may kill you.”

As you plan for retirement and venture forth into Distribution Land, you will face perils. Don’t be afraid. Be prepared. Visit www.mysecondopiniontoday.com for a free consultation and advice on if you truly are prepared with your current financial plan.

In your accumulation years, when you were adding dollars and buying equities at a bargain, you benefited from what is known as dollar-cost averaging: the technique of buying a fixed dollar amount of a particular investment on a regular schedule, regardless of the share price. More shares are purchased when prices are low, and fewer shares are bought when prices are high. Eventually, the average cost per share of the security will become smaller and smaller. Dollar cost averaging lessens the risk of investing a large amount in a single investment at the wrong time.

For example, you decide to purchase $100 worth of XYZ each month for three months. In January, XYZ is worth $33, so you buy three shares. In February, XYZ is worth $25, so you buy four additional shares. Finally, in March, XYZ is worth $20, so you buy five shares. In total, you purchased 12 shares for an average price of approximately $25 each.

Now, in retirement,as shares go down in value, you have to sell more of them from your account to obtain the same income. It’s dollar-cost averaging in reverse. Think of it as dollar-cost ravaging. See our previous post concerning this.

We each define quality of life in our own way. We each have unique goals and dreams. Economic security can buy you time to focus your attention on what matters. My goal for you is to help you understand your own definition of the good life, and then work to make your money a tool toward achieving it.

In my opinion, you need to match your assets to your aspirations; in other words, you need to plan your life and legacy so that your life savings have meaning. Your spending should support your values and priorities. Otherwise, you may be blowing through money aimlessly, or you are just trying to grow your pile bigger.

Like any journey of any distance through an unknown area, without a guide and without a clear picture of your finances, it would seem to be difficult to know for certain whether you will make it to your destination. Start your journey with a free chapter from my book DistributionLand at www.distributionland.com and start uncovering how to make your journey a safe and rewarding one.

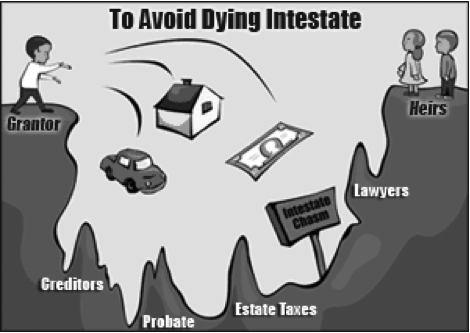

I am amazed at how many successful people, and those who have children, do not have a will. A will is a document by which a person can direct the distribution of assets when he or she dies. It is used to carry out the intention of the deceased as to who gets what. A will has many benefits. In general, it ensures that the assets are distributed according to your wishes when you die, and while you are alive it may give you a sense of comfort knowing your wishes will be carried out, or you have taken steps to put your affairs in order. If you die without a will, the state steps in and distributes your assets according to the provisions of the state. It’s called “dying intestate.”

Here are a few additional legal papers that everyone should have. Most attorneys now provide these as part of an all inclusive suite of documents:

A living will, which you can think of as your right-to-die statement. It states your health-care directives regarding life-prolonging medical treatment. If the time comes when you no longer can speak for yourself, a living will directs your family and physicians on the actions they are to take.

A health-care power of attorney, and a durable power of attorney—and these powers may be designated to different people. You may prefer that one person make decisions on the handling of your medical concerns, and you may want somebody else to have the durable power of attorney to look after your financial affairs or conduct other business for you if you become incapacitated.

It may be an emotionally challenging task to sit down and think about these matters, but having these documents in place can ensure peace of mind later on.

Mutual of Omaha Investor Services, Inc. and its representatives do not provide legal advice. Consult your legal advisor for advice regarding your particular situation.

Vanguard does a report every year called “How America Saves” on the 401(k)-type plans that it manages. The 2013 Vanguard report has some interesting insights: Thirty-two percent of employees do not contribute to a 401(k). 27 percent of employees older than 55 do not contribute. Among employees with incomes greater than $100,000, 12 percent do not contribute.

When people ask us how much they should be saving, we tell them that ideally, if they want to retire with the same purchasing power in the future as they have today, they need to set aside a minimum of 15 percent. Under the old pension system, people contributed 15 to 20 percent. Companies built that amount into the benefit package. Nothing stops people from saving at that rate today, but many may not be doing so. The picture here is pretty clear: If people don’t contribute to their 401(k)s, or if they don’t contribute enough, of course they are not going to have enough in their accounts to cover their retirement. The 401(k)s and IRAs* have pretty much replaced pensions, but people may not have the investment skills needed to deal with them properly.

For example, people often change employers so it’s not unusual for them to have multiple accounts from previous jobs. What we see is that when people change jobs, they tend to look at their account with the previous employee as found money. They withdraw it and end up paying a penalty of 10 percent, if they are younger than 59 1/2. Not only that, but there will be taxes due on the contributions and earnings of the ‘windfall’ which may also result in putting them into a higher tax bracket. The result is that they may lose 40 percent of that money. If that’s the way you save for retirement, you are always starting from zero.

*Age, income and contribution limits vary for each plan.

Sometimes you can make more money by saving taxes than you can by making more money. This is important to understand, particularly considering what is inevitable: History reflects that taxes tend to rise.

It’s important to understand the difference between taxable, tax deferred and tax-free investing. Let’s take a look at how each would affect a typical account. Suppose you started with $100,000 and added $10,000 each year for 20 years. Let’s presume a rate of return of 4 percent and a tax bracket of 25 percent.

On a tax-free account, the account value after 20 years would be $516,893.

On a fully taxable account, your rate of return is effectively only 3 percent. After 20 years, the account value would be $449,315.

On a tax-deferred account, your account value after 20 years would again be $516,893. However, you have only postponed taxes. If you now paid them all, you would be left with an account value of $462,670.

A financial advisor can help you determine which is best for your individual needs. Here is some simple advice though: You should only pay taxes on money you are withdrawing as money to spend. Otherwise, there may be better ways to manage it. Visit www.familywealthadvisory.com for more resources and start uncovering what tax strategy works best for your situation.

Mutual of Omaha Investor Services, Inc. and its representatives do not provide tax advice. Consult your tax advisor for advice regarding your particular situation.

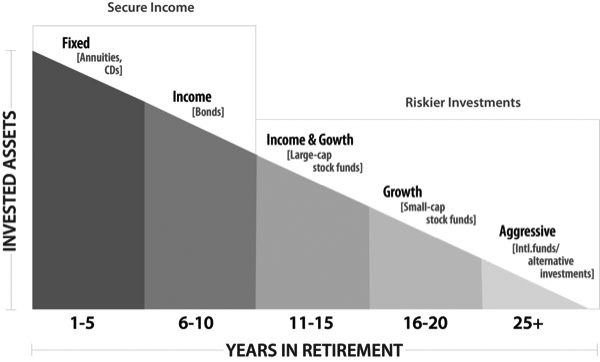

In retirement ROI stands for reliability of income*, a far greater concern in these years than return on investments. You can’t effectively chase both at the same time. But you can pursue both goals if you compartmentalize your money based on short-term, medium-term, and long-term goals.

You may have seen what is called the “risk pyramid,” rising from conservative fixed investments at the bottom to more aggressive growth vehicles at the top. Imagine that pyramid toppled on its side. You would have, at the left, the widest part—the fixed investments. At the right you would have the growth investments. This pyramid on its side is another way to visualize the time sequences in certain types of income planning.

How does it work? Reliable sources of income such as Social Security, perhaps a pension, and income from a job are calculated first. Then we put in the targeted growth rate, and we use conservative figures. Then we set up four to six segments, usually in five-year payout periods. The first bucket takes you to five years into retirement; the second takes you to ten years; and so on. This process supports the use of the Time Segment Model.

If this sounds like a good plan for your retirement needs, get in touch at www.familywealthadvisory.com for more information.

*ROI Reliability of Income is a registered trademark of Wealth2k, Inc. Used with permission.