The tactic of withdrawing from an account that rises or falls with the market can be debilitating to your wealth. You are at the mercy of sequence of return risk (the potential consequences of a bad sequence of returns) at the time you begin withdrawing money from your investments (reverse dollar cost averaging).

If those don’t drain your account, you will most likely deplete it entirely just by living too long.

Adding guaranteed income products to a traditionally diversified portfolio may provide the potential to capture a portion of market gains, while potentially limiting losses when the market experiences a downturn. Using this model, explained below, can also help.

Time Segment Model

A more disciplined structure for creating retirement income. This approach is designed to spread your portfolio across multiple accounts, each designed to produce income over a certain period of time. How each account is invested depends on how soon the money is to be used. Typically, the initial segments are for immediate needs and may therefore be allocated conservatively in fixed rate or even guaranteed investment products such as certificates of deposit or immediate annuities that may not be subject to a fluctuation in principal. Segments designated for later use can be invested more aggressively. Since they won’t be touched for a while, they have time to overcome market corrections. Over time the aggressive segments will be shifted to more conservative products as retirement savings are used.

Using this model to build your investment portfolio may allow for continued steady income instead of just playing the stock market game of chance. If you aren’t sure that your current plan uses this model, maybe it’s time for a second opinion. Schedule yours at www.mysecondopiniontoday.com for a no obligation assessment of your current portfolio.

All investing involves risk, including possible loss of principal.

Despite the risks you might now know of like, dollar cost ravaging and inflation, some advisors still put everything in a lump sum for systematic withdrawals. They will craft a portfolio that seems beautiful in its asset allocation, but really the income derives from withdrawing a percentage of the portfolio. And that puts the entire portfolio at risk.

Let’s say it’s in a 60-40 mix of stocks and bonds, and the market tumbles. “You don’t have all your eggs in one basket,” you will hear, and that’s the line of “modern portfolio theory,” which isn’t so modern anymore, having been around for 60 years or so. It came from a time when the United States was the dominant investment player in the world. Today’s global economy behaves differently. Simply put, Modern Portfolio Theory tells you that diversification leads to retirement success. But don’t feel too reassured. Diversification is too often defined as stocks, bonds and cash. In times of extreme volatility, investments get more closely correlated to one another. Often portfolios don’t include other types of investments or downside protection strategies that truly help to build a diversified portfolio. Guaranteed income products may be an effective alternative investment.

An investment strategy that requires luck—luck that you will retire into a bull market and not a bear—isn’t much better than a strategy that requires flipping a coin. An appropriate strategy for you depends on your investment objectives, risk tolerance and time horizon.

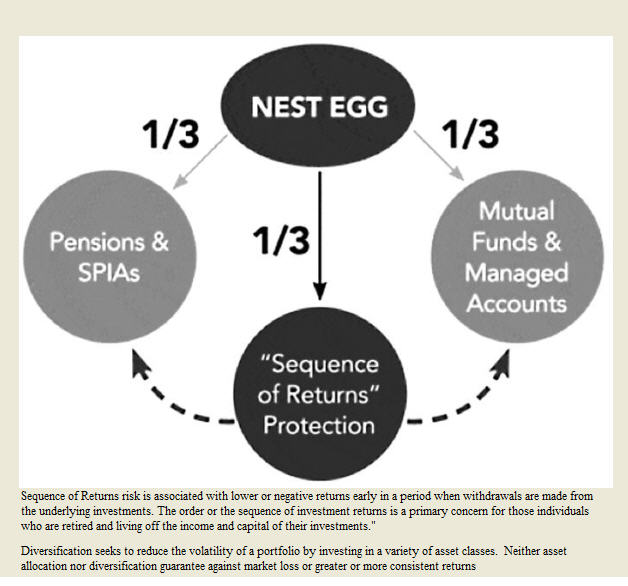

Professor Moshe Milevsky, a researcher, author, and speaker on personal financial planning, talks about not just asset allocation, but product allocation for retirement. Product allocation is the next step in the evolution of asset allocation, designed specifically for people close to or in retirement. Rather than allocating a pool of money among asset classes, you also incorporate guaranteed income products.

According to Milevsky, product allocation can be accomplished with three product silos:

Traditional Investments: These could include separately managed accounts, exchange-traded funds (ETFs), mutual funds, and other conventional accumulation-based instruments. Throughout retirement, one would systematically withdraw these assets, attempting to make them last as long as possible and then use asset allocation to achieve a desired return with an acceptable degree of risk.

Pensions and Immediate Annuities: These could include defined benefit plans and fixed income annuity products (or payout annuities). In exchange for fixed income payments, you give up liquidity, investment control, and in some cases, the ability to leave any of these assets to heirs.

Guaranteed Income Products: May offer income for life, exposure to stock market gains and losses, and control. They are also designed to leave remaining assets as an inheritance and can provide protection against sequence-of-returns risk.

How much money you should allocate to each category depends on your expected retirement age, gender, health status, desired spending rate, and inflation assumptions. For more resources to help you understand your asset allocation options, visit www.familywealthadvisory.com.

Asset Allocation seeks to maximize the performance of your investment portfolio using diversification. Although using an asset allocation methodology does not guarantee greater returns or more consistent returns, it may be able to reduce the volatility of your portfolio.

Imagine that you have a 200-piece jigsaw puzzle scattered in front of you. Where would you start? When I ask people that, most say they would start at the corners where they figure it’s easier to piece together all those interlocking shapes. Likewise, many people just dump their box of investments on an advisor’s table and shift them around, trying this investment here, and that one there, and hoping that eventually things might fall into place.

But how about first taking a good look at the picture on the cover of the box? Before you start working on the pieces, you need to have the big view. You should work with an advisor who will make sure you get the perspective you need so that your investment strategy makes sense for you and is designed to advance your goals.

Finding an advisor you can trust to give you direction, not just do what you ask, may result in a much more secure retirement future. Is your puzzle pieced together with the big picture in mind? Consider getting a second opinion on your current investment portfolio and schedule a free consultation at www.mysecondopiniontoday.com

“Many people are so occupied with getting out of a career trap that they seem to care little about what happens after they leave their jobs. Too many people retire to nothing and then wonder why they feel empty and disenchanted.” From “Comfort Zones”, by Elwood Chapman and Marion Haynes

The point being, if you would like to avoid feeling empty and disenchanted, you shouldn’t just wing it. Yet it seems that is how a lot of people approach retirement. They wait until they’re into it before they start planning. As a result, things may not work out as well as they would if they had addressed them earlier, and they can end up unhappy and disillusioned. They had grown weary of the daily race of their workaday life, but they may find retirement filled with new anxieties. They can’t seem to slow down.

By deciding your destination up front, you can set your own pace. You will know how much income you need to accomplish your goals and still live comfortably the rest of your days. The “Retirement Red Zone,” as Prudential calls it, should begin five years prior, and probably ten years if you are a business owner. Many people have an investment plan but no overall financial plan.

Visualize the lifestyle that you will find most satisfying and fulfilling. Give your life direction by setting goals so you can anticipate, plan and prepare. Focus on expectations. Start now; download a free chapter of my book DistributionLand (www.distributionland.com) for the strategies and risks to consider as you begin the journey.

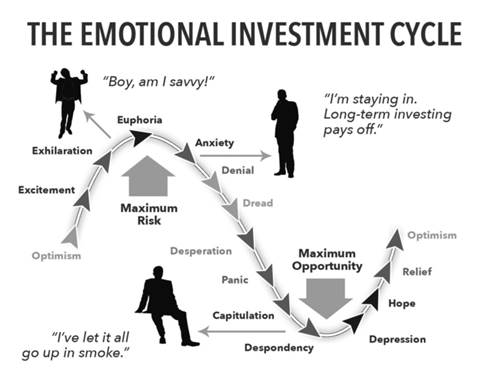

At Family Wealth Management, what we want individuals to do is seek to identify, understand, and manage risk by focusing on investment vehicles that offer a higher potential for lower volatility, better downside protection, and consistent compensation for the risk they are taking. People are not often focusing on lower volatility and downside protection. They’re just focusing on higher potential return, fueled by emotions or quick reactions.

Market analysis over the past century has shown that extreme changes in investment markets represent only about 3 percent of the time line*. What has made money for investors in very good markets has happened only 3 percent of the time and what created catastrophic losses also happened only 3 percent of the time. But, when those times hit, emotions run high and mistakes can be made due to those emotions and desired market performance.

That’s why it is important to work with an advisor who will work with you to help avoid this potential mistake and keep your emotions from getting the best of you. People sometimes panic and pursue high-risk interest rates, believing that is their only choice if they are to survive. It’s not the case. If you have a written retirement income plan, you will be able to see that.

*White Paper by Aftcast in 2010 titled “Lifelong Retirement Income: Cost of Excluding Variable Annuities”

People sometimes don’t even know, or they have only a vague idea. They’re not even sure of the scope of their assets. If you don’t know where your documents are, you’ll be leaving a mess for those who try to pick up the pieces when you are gone.

Coordinate and simplify your affairs through a written financial plan. Used in conjunction with an online financial center or service, where all of your assets and debts, bank accounts and mortgages, and more can be updated daily, you will be leaving things well in order.

For example, at Family Wealth Management we give our clients an online vault and scan everything into it, including wills and trusts and powers of attorney, property deeds, passports, birth certificates, and more. It’s all in the vault. It’s set up for access by your chosen executor or trustee upon your passing and is part of our “Total Client Profile.”

At the very least, you will want to create a document that lists everything important that you can bring to mind. There are online services that can help you, or just grab pen and paper and start writing. Who are your advisors? What are your assets and debts? Who carries your life insurance? Who should be contacted? What papers do you keep where? You’ll want to keep that list with your will or trust papers, and perhaps give it to your executor or your children in advance.

We believe these are the three fundamental aspects of money management. A sound retirement plan must provide a good balance of all three – safety, reliable income; liquidity, so that cash is accessible in emergencies; and growth, so that you beat inflation, grow your portfolio to replenish income needs, and leave an inheritance.

What might a good balance include? Liquid investments may include cash, savings, and money market accounts. Low-risk investments may include short-term bonds, insurance products, and bank certificates of deposit. Slightly more aggressive, but still reasonably conservative choices, include fixed income investments, such as corporate or government bonds. Growth investments could include individual stocks and real estate, for example.

Make sure that your retirement plan is well balanced. Schedule a free consulting session at www.mysecondopiniontoday.com for a cup of coffee and second opinion on your current path to retirement.

“What a man really fears is not so much extinction but extinction with insignificance.”

Ernest Becker, the Pulitzer Prize-winning psychologist and author of The Denial of Death

My father fought in the Battle of the Bulge, and when I was a young boy I heard a lot of his war stories. They really got me interested in history and the world wars, particularly World War II. When both of us knew that he had a limited time to live, I asked him to get deep and narrow with my two boys about his experiences so that they could have a personal and intimate understanding of their grandfather and what he had endured. They are in their mid to late-20s now, and they are enthralled with history and virtually anything that has to do with the Second World War. Their grandfather left them a lasting legacy. He is forever vivid in their minds.

How many people know anything about their great grandparents or their great, great grandparents? It’s as if memories fade to oblivion after a few generations. In legacy planning, we tell people there comes a time in life when you long to know that you had some purpose. You want to know that you are leaving a meaningful mark in the world.

It goes beyond wills and estate planning. Creating a legacy plan starts with a “bucket list” of the lifetime achievements that you desire, and it helps you to express your values and interests—what truly matters to you. You can document the essence of your life as a priceless bequest to your survivors.

A truly diversified portfolio isn’t a mix of stocks and bonds, but rather it includes some genuinely conservative investments that were created for Distribution Land. Why? Because stocks and bonds are subject to constant highs and lows, these fluctuations aren’t well tolerated by a portfolio where money earned is used as income rather than savings.

In my opinion, other types of investments should supplement stocks and bonds, like insurance products for example.

Professor Moshe Milevsky, a researcher, author, and speaker on personal financial planning, talks about not just asset allocation, but product allocation for retirement. This asset allocation chart, created by Professor Milevsky, shows allocation includes insurance annuities, life insurance, and other products.