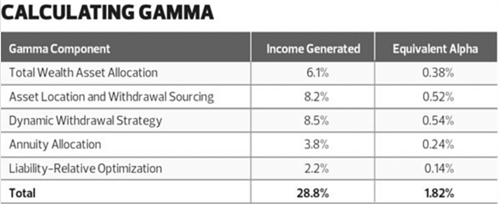

How do you know you are getting smart financial advice? Can financial advice be quantified? A new Morningstar approach may help you put a value on the value of an advisor. Researchers at Morningstar have devised what they’re calling gamma to quantify the benefit planners can deliver to clients.

Gamma is defined as the additional value achieved by an individual from making more intelligent planning decisions. According to Morningstar, planners can add the equivalent of a 1.82 percent annual arithmetic return to clients through five components of gamma. Over time, that can translate to nearly 29 percent more that clients can spend in retirement.

Morningstar research executives David Blanchett and Paul Kaplan list five components of client service, which make up gamma. None of these should come as much of a surprise to a good planner:

Total wealth asset allocation

Tax efficiency

Dynamic withdrawal strategies

Annuity planning

Liability-relative optimization

If you feel your current financial advisor is missing the mark, visit www.mysecondopiniontoday.com for a free no obligation consultation to review your current portfolio and goals.

If one or two of those terms seem opaque, you’re not alone, so below are details on the actions and services planners should be providing to clients in each of the five areas, as well as a few others. According to Morningstar, each of these components is worth a certain percent more each year and a cumulative amount over time.

You have dreams and goals for your retirement. The challenging part is uncovering if whether your expressed goals are realistic and attainable or not.

One couple came to my office saying they wanted to retire in about five years, at age 60, and they wanted to pay for the kids’ college educations, and they wanted to pay for two daughters’ weddings. “Those are noble goals,” I told them, and I figured they must have the assets to handle them. But all they had was $50,000 in an IRA. I gave them the bad news: They would need to keep working, and they couldn’t afford those tuitions and weddings.

When people hear that, they sometimes search for somebody who tells them otherwise and will validate their opinion. And then they may enter dangerous territory. Never forget: Fearsome creatures can get you in Distribution Land. Visit www.familywealthadvisory.com for more information on how to start laying suitable plans for your future.

Your financial planner should be in the business of helping people thrive in retirement, not patting their backs as they head into peril. That’s why so much emphasis should be placed on defining goals and organizing life priorities; that’s one of the best ways for you to organize your finances.

Planning for unforeseen circumstances is a large part of thriving in Distribution Land. That’s probably a shift from what you are used to because previously there was time to recover if a circumstance arose that impacted your financial situation. But in retirement, things change.

What about the retired couple who get a phone call one day from their daughter—her husband has left me, she cries, and may I come home with the kids and the dog? All of a sudden they’re buying food for six instead of two, and replacing the carpet.

Or maybe it’s you who are getting the divorce; the rate among people in their 70s is higher than ever*. It doesn’t take much imagination to see what that does to a retirement plan.

Life situations, in other words, have the power to propel you prematurely into Distribution Land, or send you packing back to Accumulation Land. But most all of those situations can be anticipated. You may be able to head them off at the pass.

Retirees need specific advice on longevity planning, managing withdrawals from retirement funds, transferring wealth to heirs, and many other complex issues besides how to allocate their assets. Too often, the focus is on the money and not the humanity.

Jerry seemed so eager to retire after a 35-year career. Jerry and his wife, Jean, moved to Florida. Later, in retirement, he came in for a visit. “If I knew this was what it was going to be like, I’d have never retired. I hate every minute. I hate it in Florida.”

Jerry was unhappier than ever. He thought retirement was going to mean his freedom. What it meant was that he abandoned the little bit of stability he had. And he didn’t have enough money to take his boat out fishing—and that’s his main hobby. He had a pension and a decent amount of money, but he and Jean still felt strapped.

Jerry’s strategy was to spend as little as possible and let the savings grow and also delay his Social Security so that they would have more later—or rather, so that Jean would have more later. He wanted to make sure Jean would be all right without him.

This is an often-typical retirement story. Americans are retiring by the millions, and many others are coming to see that it’s crucial to carefully plan for retirement. So many people pull up their roots in retirement and leave their whole social circle. They start anew, far from home. No longer are they near friends and family. No longer do they see their acquaintances at work. If their career has ended, they may feel they have lost a sense of purpose.

In addition to a whole new lifestyle, fear holds so many people back. Some even hoard, fretting unnecessarily, while others seem oblivious about very real dangers they are facing. It goes both ways. The point is that you may need help. Visit www.distributionland.com for a free chapter of Distribution Land, and start to understand what you need to consider first as you enter retirement. You need to be able to get a grip on what your financial state truly is. A professional advisor can work with you to help you pursue a pleasant and stable retirement in an effort to avoid a situation like Jerry, unhappy and unsure of your retirement future.

When seeking the services of a financial advisor, you aren’t just finding someone to manage your money; you are finding a partner to manage your future and your legacy. That’s a big deal. It involves more than just a directive about growth percentages or investment numbers; it should start with your priorities. You, your spouse, and your family are the client, not just your money.

Thinking through these matters of finances, dreams, priorities and concerns is paramount, particularly as you and your spouse plan together. A good advisor should strive to understand his or her client’s and even help to uncover priorities and goals before crafting a financial plan for retirement. An advisor should help you identify how you feel about money and what you believe it should accomplish.

The right questions that you should be asked examine your past, present and future as well as at the roots of your relationship with money. What were your first experiences with it? What was it like in the household where you grew up? The advisor should ask to hear from both husband and wife. This helps to ensure both are on the same page and helps to see areas where each thinks about money differently so the advisor knows how to approach building a plan that works.

I have seen it all – couples that have had all the right discussions and know what the other wants and others who through the process learn a lot. For example, as I talked with one couple, the husband told me about his dream of cruising around the Keys in a sailboat and visiting the islands. “I’m not doing that,” his wife said. “I get seasick. No way.” Wouldn’t you think they would have already talked about that? But it’s not unusual for one spouse to look at the other and say, “I never knew you thought that.”

Start with your priorities, individual and shared. It will help you and your spouse make the right financial decisions later on and allow the advisor to structure your retirement around those shared priorities.

Managing risk. It’s at the very heart of what a financial planner does. As you get closer to retirement, you need to insulate yourself from what the market can do to your portfolio, but you still need to have enough growth to keep in front of inflation and provide sufficient income to pursue your established goals.

If you don’t take care, you can blow your nest egg. One way to do that is to ignore inflation. I meet with many clients who have trouble understanding that. They figure that if they can get a certain percentage off their account, they will be fine. I point out that they’ll likely be living off that money for decades to come. Things will inevitably cost more; think of how much they cost in, say, the 1960s compared with now. A retirement plan should account for the need to have an income that keeps pace with inflation. If it’s time to reassess your current retirement plan, visit www.mysecondopiniontoday.com for a free consultation and review to make sure your plan accounts for all risks, even inflation.

Finding the right Financial Advisor to be your guide through Distribution Land is extremely important. How can you be sure whom you are dealing with? How do you know who will have that fiduciary responsibility to watch out for you? To get you started here are 5 questions to ask or check for as you begin your search:

1. Does the advisor have a CFP Designation? Those with a designation of CFP (Certified Financial Planner) are required to follow a code of ethics. They are subject to regulation by various federal, industry, and state agencies. Your best choice is to limit your risk and work with somebody with an obligation to abide by a code of ethics—a Certified Financial Planner.

2. Who Holds Your Money? It seems like a simple thing, but it’s easy to overlook. You want to have your money held by a custodian, like Pershing, LLC or Fidelity Institutional Wealth Services. If you were to have an advisor named, for example, Bernie Madoff, you don’t want to see “Bernie’s Excellent Investment Firm” stamped on your statements. Be aware of just who has your money.

3. Can the advisor provide a copy of his/her ADV Part 2B? This disclosure form holds a few key indicators. It will help you distinguish whether the advisor is fee-based or not. This report also discloses if there has been certain disciplinary history. Be sure to utilize other resources, such as SEC (www.sec.gov/investor/brokers.htm) and FINRA (www.finra.org/Investors/ToolsCalculators/BrokerCheck/), to run checks for complaints against the advisor whom you are considering as well.

4. Is the advisor an employee of a financial firm or working independently? Some advisors who work for a firm offer proprietary products, and they may have to sell certain products and meet minimums. Their primary objective may be to make money and limit their own risks. Look instead for independent advisors. That doesn’t mean they don’t have relationships with certain firms, but they are paid as independent contractors.

5. Does the individual have a specific process or approach to advising? If the advisor can’t produce a process, or if it’s all investment related and focused on money, be wary. What you want to see is a process that is centered on you, with the money there to support you.

I often use the analogy of sailing and rowing to explain how to manage money wisely. There are two strategies for sailing, when you are making the most of a favorable wind. There are two other strategies for rowing, when you are trying not to fall behind and lose your way in a storm. The rowing strategies aim to get a return through most market cycles. They are designed to manage the volatility better. A good portfolio is going to have a combination of all four of these strategies.

The two sailing approaches are called “strategic,” and “tactical constrained.” The former calls for a fixed balance of stocks and bonds to weather any storm. The latter adjust those percentages depending on market conditions. The adjustments are tactical, but they are constrained within boundaries. They can only go so far.

The two rowing strategies are “tactical unconstrained” and “absolute return.” The former doesn’t have those constraints that I just mentioned. The latter is based on getting a return during any market cycle, using such tactics as short selling and buying alternative investments.

Many investors will use a combination of those strategies, weighted toward whether their aim is to accumulate assets or preserve and distribute them. The balance of strategies also will depend on the market outlook and their risk tolerance—is the investor aggressive or moderately conservative?

“Do you have a written plan forecasting income and expenses in retirement, designed to analyze whether or not you may run out of money?”

You need a financial plan in place while you are alive and for the sake of your loved ones when you are gone. It eliminates guessing. It is indeed the fear of the unknown that can hamstring you in retirement. Whether it’s founded or unfounded, it comes down to uncertainty. Without a financial plan, you don’t know whether or not you could fend off a real threat, and you may imagine a threat that doesn’t exist and therefore spend years scrimping. You deserve to enjoy life.

Imagine if you will, a couple in their 70s, in the early stages of their financial planning, and the wife is upset. She wants to go on vacation every year, but her husband insists they don’t have the money. She wants a professional to weigh in.

It would make sense to prepare a cash flow analysis and income projection and talk to them about how much they thought such vacations would cost. The answer may be right there in black and white. Perhaps there is no reason why they shouldn’t be taking yearly vacations.

And that’s the real purpose of a financial plan. People feel frozen when they don’t know what the future looks like. A couple may feel they need to hoard their money and not enjoy it, or at least one of the spouses feels that way. Next thing you know, one of them is too sick to go anywhere and they haven’t done anything. Put a plan in place so that you can go out and enjoy the fruits of your labor.

No doubt you have seen the acronym ROI, for return on investment. In Distribution Land, however, ROI stands for reliability of income. The conventional investment wisdom that may have served you well during your wage-earning years should be replaced with a more mature wisdom befitting this stage of life. You have a lot more to consider besides just the return you can get.

What you need is what many people lack: a written plan that forecasts retirement income and expenses to project how your savings can support your spending so that you can make intelligent decisions.

And you need to talk through what you envision for retirement—where do you want to be, why do you want to be there, who do you want to be there with. How do you feel about being retired? Do you have any concerns or fears? A retirement plan isn’t just about managing money. It has to coordinate your money with your life.

Let’s say that sitting in front of you is a 1000 piece jigsaw puzzle. Where would you start? Most say on the edges or the corners. But what if you started with the picture on the cover of the box? Why? Because until you know what that picture looks like, all you’re doing is moving pieces around with no goal in mind.

Creating a unique plan requires finding the right balance of hopes and dreams, the desired lifestyle, and the income needed to support it. It requires investing for a target income while still commanding a return that beats inflation. Determine whether they are being realistic. If your asset base is relatively modest, you cannot take lavish vacations, support multiple charities, help all your children, play golf daily, and still have enough income for the rest of your life.

Need some advice and guidance? Go to www.distributionland.com for a free chapter of my book Distribution Land: A Retiree’s Survival Manual for Transitioning to a World of New Rules & Unexpected Dangers.

How do you know you are getting smart financial advice? Can financial advice be quantified? A new Morningstar approach may help you put a value on the value of an advisor. Researchers at Morningstar have devised what they’re calling gamma to quantify the benefit planners can deliver to clients.

How do you know you are getting smart financial advice? Can financial advice be quantified? A new Morningstar approach may help you put a value on the value of an advisor. Researchers at Morningstar have devised what they’re calling gamma to quantify the benefit planners can deliver to clients.