An accountant and his wife recently came to my office to prepare for their retirement in a few years. They had about $2.5 million in CDs and bonds, and they had figured out how much they wanted in retirement income. They presumed all was well. But my projection showed their portfolio in a death spiral by their early 80s.

“You know what that means, right?” I asked them. They risked running out of money.

“Yeah, it means I don’t believe it, how’s that?” the accountant said.

I showed him the numbers, and as a CPA he understood them, yet couldn’t quite grasp why this would be happening.

“Have you ever seen Jurassic Park?” I asked him.

“Sure. Dinosaurs gone bad.”

“Right. Remember the scene where the boy tells the archaeologist he wouldn’t be afraid of a raptor?” I asked. “The guy shows the kid a petrified claw and demonstrates how a raptor could shred him to pieces. But then he explains that the raptor that would be staring him down wouldn’t be the one he’d have to worry about. In fact, he wouldn’t have to worry about him at all. See, Velociraptors hunt in packs and it’s the ones to the sides that are going to kill you, and you’re never going to see them coming.”

The CPA furrowed his brow.

“You were scared,” I explained, “because you saw that market risk in front of you, staring you down. So you put all your money into CDs and bonds so you wouldn’t have to worry about market risk. But off to the side—and I don’t think you see it coming—are inflation and longevity as well as other risks that may kill you.”

As you plan for retirement and venture forth into Distribution Land, you will face perils. Don’t be afraid. Be prepared. Visit www.mysecondopiniontoday.com for a free consultation and advice on if you truly are prepared with your current financial plan.

Throughout your search and preparation for retirement, you might have heard of the Rule of 100, which suggests that if you subtract your age from 100, the result is how much of your portfolio should be invested in stocks, with the remainder in bonds. Presumably, that would keep your investments diversified.

However, that’s not true diversification. If you have everything in stocks and bonds, you still have all of your assets exposed to some levels of risk. In my opinion, rules of thumb such as that will generally hurt you more than they will help you because they are an attempt to apply a general principle to highly individual needs and wants. Should everyone age 76 have the same portfolio? No, that’s quite the opposite of diverse, not mention no longer realistic as the market and interest rates shift.

To provide some background information, the bond market is not a world of safety. Here’s what people don’t realize: We have just gone through a 30-year bull run in the bond markets 1. In 1981 you could get CDs for 16 percent; now, the rates are 1 percent or less. These are the lowest interest rates people have seen in their lifetime. Why were the bond markets so attractive in the last 30 years? Because as interest rates go down, the price of the bonds appreciate. It was a great place to obtain some safety and catch a wave for three decades.

Today, with money market rates near zero, one could assume that rates cannot go down much further and that they likely will rise as some point in the future. As those rates rise, what will happen to bond values? They will fall. Rising rates equal falling bond value, just as falling rates equal rising bond value. This is no longer a conservative and lucrative approach to diversification.

So what is a diverse portfolio for today’s retirees? Professor Moshe Milevsky (The IFID Centre, York University Toronto), a researcher, author, and speaker on personal financial planning, talks about not just asset allocation, but product allocation for retirement. A truly diversified portfolio isn’t a mix of stocks and bonds, but rather it includes some genuinely conservative investments across several specific asset and insurance areas.

6 “PIMCO’s Gross Says Bull Run in Bonds over.” Reuters. Thomson Reuters, 10 May 2013.

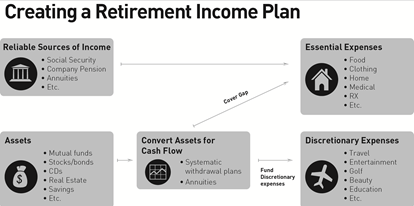

Ideally, you need to know if you have enough assets and investments to retire happily and safely. Here are the first three steps you and your financial advisor should take:

Step 1: Estimate how long retirement income will be needed. How many years must the assets last? Are you and your spouse healthy? Is there a history of longevity in your family?

Step 2. Identify and manage the numerous risks, such as inflation, longevity and healthcare expenses, just to name a few. then try to reduce the risks, as much as possible,

Step 3. Start to convert resources into income, regularly updating the plan. Converting assets for lifetime income is the fundamental strategy in the retirement income planning process.

To get a ballpark figure, you can use this standard approach to calculating income needs: (1) figure average monthly expenses, (2) add up any lifetime income such Social Security and pension, and (3) subtract the monthly income from the expenses to determine any gap. To see if the gap can be filled, add up all financial assets and multiply by an expected annual rate of return, then divide the result by 12 for a monthly income stream. If it fills the gap, you can retire.

If it doesn’t fill the gap, look at some other approaches. You have various options: Increase your returns where possible; find other lifetime income sources; spend less in retirement; work full or part time; postpone the start of Social Security or pension payments; increase your savings; or tap into your home equity.

Of course, your financial advisor is there to help you determine the best course of action for maintaining your income stream or uncovering ways to increase that income stream for the right retirement plan for you.

In the next 15 years or so, baby boomers will be retiring in droves, with fewer and fewer workers to support them in the Social Security system. The government’s spending for Social Security will rise faster than tax income because the population over age 65 is growing faster than the working age population based on 2007 Social Security Annual Reports1.

The country faces not only a tide of baby boomers but also an increase in life expectancy. In 1935, when Social Security began, retirement lasted but a few years. Today it lasts a few decades and longer. For a couple both aged 65 today, according to projections, there’s a 50 percent chance that one will live to 92 and a 25 percent chance one will live to 97. The population is aging 2.

These days, from a financial standpoint, the primal fear often is not that a retiree will die too soon, but rather that they will live too long. This shouldn’t be a fear but rather cause for celebration! Change your outlook simply by preparing wisely for your retirement future – establish your priorities, find the right financial advisor, plan for possible detours – enjoy the ride.

1Social Security – ssa.gov/history/pdf/tr07summary.pdf 2 American Council of Life Insurers – acli.com/Tools/IndustryFacts/LifeInsurersFactBook/ Documents/FB11Mortality.pdf (11/18/2011)

Distribution Land is totally different than what you’ve experienced. To this point, you have been in Accumulation Land, where time has been your friend. You were likely advised to put money away consistently. You weren’t too concerned about whether the market soared or sagged; if it went down, it meant you could buy a greater number of shares at a bargain price. You were not planning to pull out the money soon for income.

Now you are crossing through the mist into a new world, everything looks different. Now you are withdrawing money for income, and time may no longer be your friend. If the market drops while you are pulling from your portfolio for your income needs, you could be in trouble. You might not be buying any more shares at a bargain; rather, you could be forced to sell at just the wrong time—and you don’t have years stretching ahead of you for a recovery. What you did before might not work anymore. In this land, you need different weapons for survival.

Managing risk is the most important aspect of good retirement planning, not pumping up your investment return. Retirement is no longer as simple as signing up for Social Security, collecting your pension, and settling back. Rather you are preparing for a new phase of life and dealing with different factors that contribute to that way of life. For example, you are most likely planning to be more active, will live and work longer, and, for income, need to rely more on what you’ve saved. And that means ensuring that this income has the potential to last for your lifetime and to weather rising health care expenses, inflation, and market ups and downs.

Help ensure that you are on the right track for an optimal trip through this new land. Strive to avoid pit stops and potential dangers by educating yourself and surrounding yourself with a team of professionals for your needs. Make strategic partnerships to provide guidance along the way – don’t go it alone. Wonder where to start? Visit www.mysecondopiniontoday.com for some free advice on if you are headed in the right direction.

I would like to share a story with you.

I would like to share a story with you.